Republicans have been waiting a long time for this moment. They have tried, time and again, (and again and again!) to repeal Obamacare. Now at long last, after sixty previous attempts to overturn the Affordable Care Act, commonly known as Obamacare, their moment has arrived.

President-elect Trump has made it clear that overturning the law would be a priority, as has Paul Ryan. We all watched the surreal and awkward moment, when the current President welcomed into the White House the man who would be responsible for overturning what he thought would be his legacy. President elect Trump believes that he can repeal Obamacare and return premiums to their previous levels. But I think Obamacare will live on in one form or another, here’s why.

- Millions will lose health insurance.

Before Obamacare took effect, nearly 20% of the US population did not have health insurance. The number of people who had access to insurance through an employer had been steadily dropping, the drop disproportionately affected low income levels. Those are the exact people who the law targeted. You know those people, you are those people. Working 2 or 3 part time jobs in our new economy and getting health insurance from none of them, yet being too “rich” to qualify for Medicaid. Either through exchanges, through Medicaid expansion, or through young adults on their parents’ plans, Obamacare now covers about 20 million people.

What does it sound like when 20 million people lose health insurance? Hand clapping, vigorous hand shaking, and hugs.

2. Removing “The Mandate” won’t work.

The requirement that people purchase health insurance is reviled by many, on both sides of the aisle, and was the cause of a failed supreme court challenge.Yet, over the years the rhetoric has changed from “repeal” Obamacare to “repeal and replace”. Why? As unpopular as the mandate is, some parts of Obamacare are actually pretty popular. Like how insurance can no longer weasel out of covering kidney stones because you having kidneys was a pre-existing condition (true story!).

If President Trump cherry-picks these good parts and removes the mandate he is going to be accomplish one thing: He’s going to jenga the heck out of America’s private insurance market.

Why? Insurance can only be as cheap as the people in the plan. If you remove the mandate forcing healthy people to purchase plans, the costs will continue to increase, and that “death spiral” that Republicans keep talking about is going to become their problem.

3. Your rising insurance premiums: It not Obamacare, it’s Epipens.

Ok, that was a catchy title, but I can’t really pin this one on Mylan, though I really, really want to. The truth is that premium increases– perhaps the very thing thing that spurred many to go to the polls– have very little, if anything to do with Obamacare. The real reason behind the increase in our health premiums is simple; our health care system is just too damn expensive. The rise in medical costs has far outpaced wage increases for the last few years. My own health care premiums and deductibles started jacking up beginning the year before Obamacare took effect, and have continued to rise since then, as likely yours have too. As much as we would like to believe it to be so, there is simply no rule or regulation within Obamacare that would cause these increases in costs. But there are plenty of new technologies that would.

Right now, hospitals all over the country, are replacing their CT scanners with newer ones that are much more sophisticated, more precise, and significantly shinier. Oh they’re also a hell of a lot more expensive, too. Ask any radiologist worth their chops and they’ll tell you that the newer machines are not truly necessary. So why are they changing them? So they can advertise to you, dear patients, that they have the best new technology. Multiply this technology factor by dozens of departments and again by thousands of hospitals, clinics, and medical offices across the country and you start to get the gist of what I’m talking about here.

But actually you still haven’t. Because while you’ve heard of epipen, you haven’t heard of the numerous other drug makers who are busy rebranding, repackaging, and reinventing their old medications so that they can re-patent them and hit you right where it hurts the most. The crotch. Oh you thought I was going to say something else there? No, they are all trying to intentionally kick us in the collective crotch. How else were they supposed to grab your wallet? It’s at that moment, that you get a letter from your insurance company stating that your insurance premiums, copays, and deductibles have increased for the fifth year in a row. And that’s when know this game of Roshambo is in full swing.

4. Medicare is running out of money.

Medicare payroll taxes by themselves don’t cover the full costs of inpatient care, the medicare trust fund is the emergency piggy bank that fills the gap. As it turns out, that emergency is now, so consider the piggy cracked. Once this fund is exhausted, sometime around 2028, seniors will be forced to accept a reduction in coverage or an increase in costs. In effect they’ll have to think twice about picking up the phone and calling 911 for that rising pain in their chest. Do they make the call or do they make rent? It’s interesting that this prospect was never brought up in this election cycle. Why is it interesting? Because, in a hailstorm of irony, Obamacare which was the very thing that drove many seniors to vote for Mr. Trump, is also the very thing that prevented that scenario from playing out. Before the enactment of Obamacare, the trust fund was estimated to run out, um, well right about now, actually. If President Trump repeals Obamacare he could effectively move this Medicare calamity to sometime in his first term.

5. The Obamacare seeds have already been planted. And they’re growing.

Many of the programs initiated under Obamacare have already made their way to the larger part of the health care economy. Given the dramatic increases in health care costs over the years many insurers are now demanding that health care providers be increasingly paid by the quality of their performance rather than how they are now, by the number of billable tasks they perform. This movement has become part and parcel of the landscape and is only going to become more entrenched as insurers struggle to snatch control of health care costs away from providers and the current fee for service system. While many of these measures are not unique to Obamacare, (actually many have nothing to do with Obamacare) they will continue on in many insurance plans both government and private.

6. The replacement will still be called Obamacare.

It is very likely that any new plan which President Trump and the Republican congress put forth will continue to have many of the consumer-friendly benefits of Obamacare.They will also find that the thorns are exceedingly difficult to remove, thus it will still have many of the problems that Obamacare has, including high premiums. But here’s something to consider regardless of what plan they put forth; The public has seemingly embraced the idea that pretty much every change in their health care is due to Obamacare. So here’s my bold prediction: no matter what they call the new plan, the public will still, some endearingly, some angrily, call it Obamacare.

7. Health care has gotten way too expensive. And we have nothing to show for it.

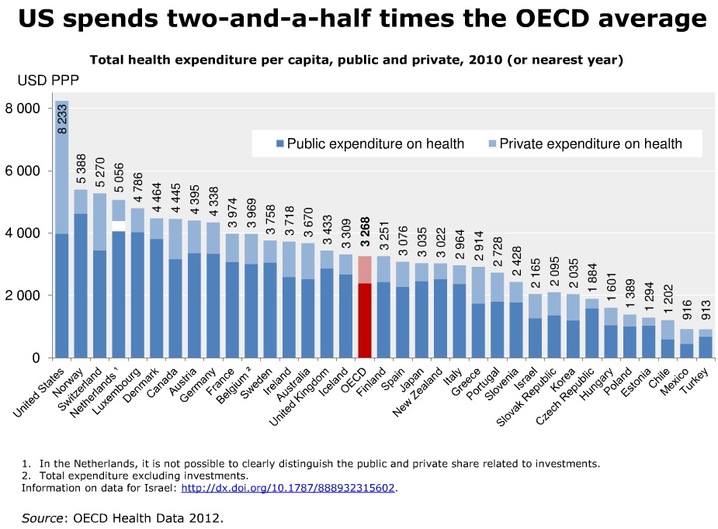

You’ve all heard the numbers, we spend about 2 and a half times as much as other industrialized countries on health care. It’s obvious to everybody that we’re doing too many humanoscans, prescribing too much Godzillamycin, and inserting far too many doohickeys into our patients’ whatchamacallems. And yet, despite this intensive over-care, we don’t live any longer. Actually our overall health is worse than most other advanced nations. It’s not just insurance companies that are up in arms. The employers that pay for the health care are fed up too, and they are demanding safer and cheaper care from health care providers. Those increasing pre-authorizations, co-pays and deductibles you’re seeing aren’t Obamacare, they’re really a reaction to try to quell that kick in the crotch we were talking about earlier. But again, most people perceive that these changes in their insurance are somehow related to Obamacare. The increased costs that insurance companies are passing on are really an attempt to make you part of the decision process. They want to make you think twice about asking your doctor about a commercial that told you to “ask your doctor” about something. Or rather after you ask your doctor about it, think about your copays and how much more expensive this treatment will be. Then ask your doctor if it’s better than the alternative. And when your doctor says “Meh, don’t know but they bought me lunch”, probably just forget it and move on to that other question that the next commercial was telling you to ask. The reality is that the vast majority of the health care changes we’ve seen in the past 5 years have more to do with new rules imposed by insurers and employers to reduce health care cost than rules imposed by Obamacare. This new cost sensitivity is entrenched in the marketplace and will be for the foreseeable future irrespective of what happens with Obamacare.

Ultimately Obamacare has been a relatively small part of a continuum of changes that are taking place in health care. And if you’re balking at my description of Obamacare as a small change, that only means you don’t know what’s coming. These changes are due to the reality that health care has become unsustainably expensive and despite all our spending we are not any healthier because of it. Future changes will continue the transformation of the healthcare market until this explosion of cost has been brought under control. And until they are, your health care premiums will continue to increase, regardless of who’s name is associated with the health care bill.